|

| [source] |

Methods of Estimating Inventory

There are two methods for estimating ending inventory:

1. Gross Profit Method

2. Retail Method

2. Retail Method

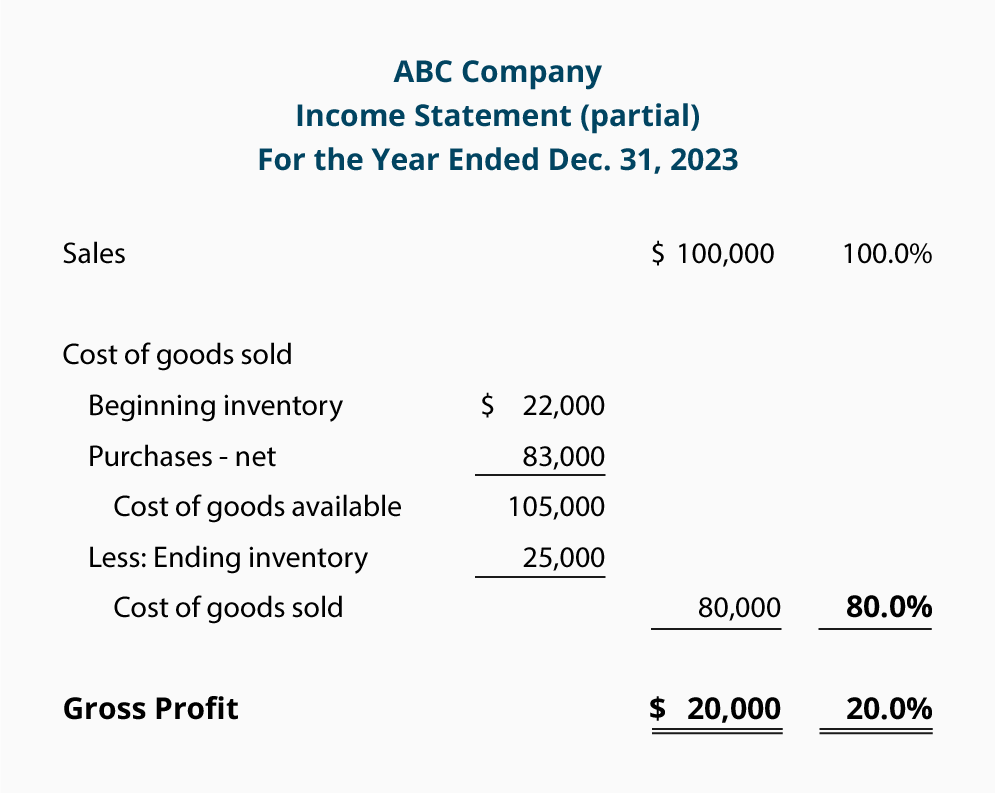

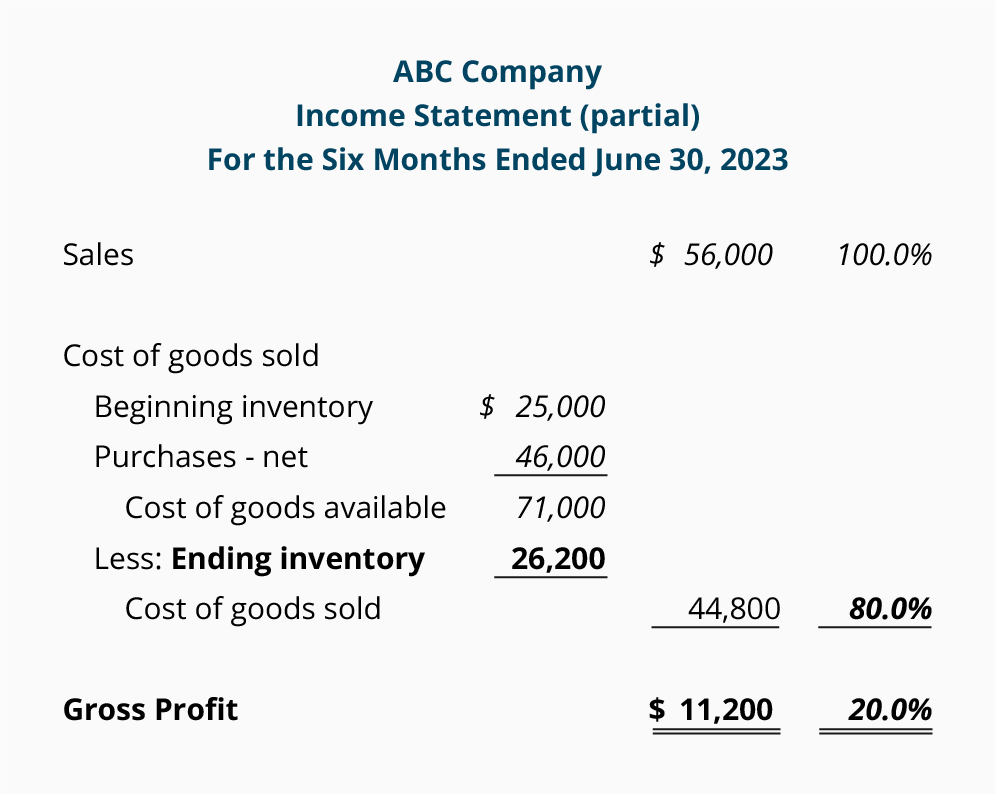

1. Gross Profit Method. The gross profit method for estimating inventory uses the information contained in the top portion of a merchandiser's multiple-step income statement:

Let's assume that we need to estimate the cost of inventory on hand on June 30, 2012. From the 2011 income statement shown above we can see that the company's gross profit is 20% of the sales and that the cost of goods sold is 80% of the sales. If those percentages are reasonable for the current year, we can use those percentages to help us estimate the cost of the inventory on hand as of June 30, 2012.

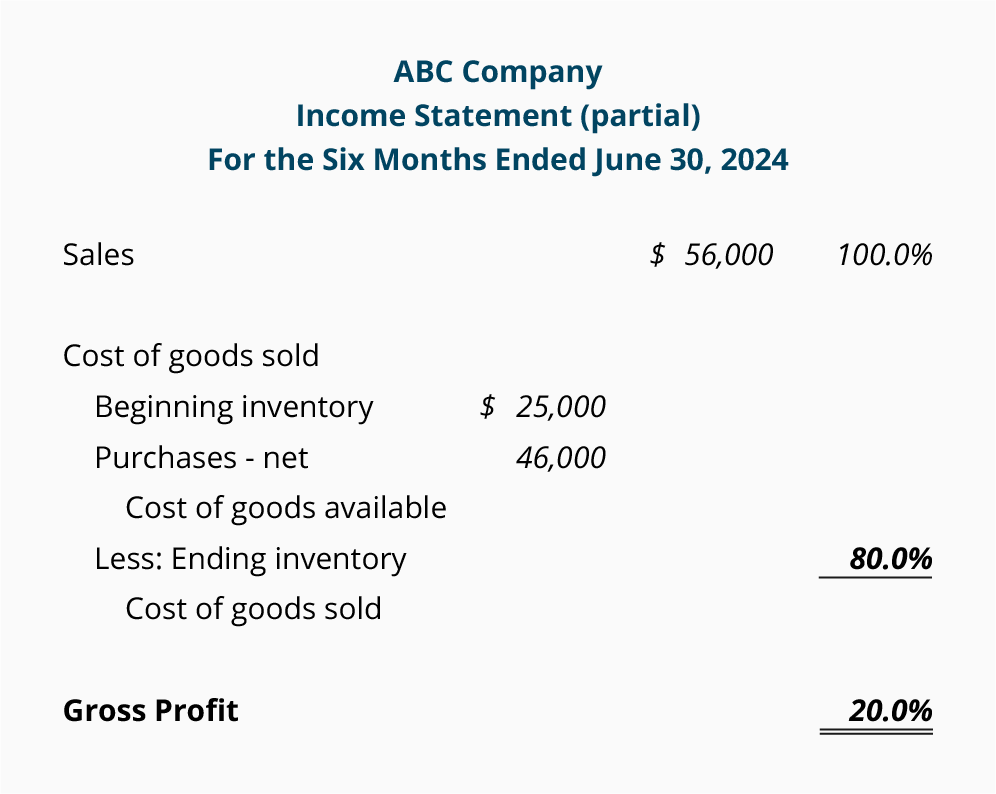

While an algebraic equation could be constructed to determine the estimated amount of ending inventory, we prefer to simply use the income statement format. We prepare a partial income statement for the period beginning after the date when inventory was last physically counted, and ending with the date for which we need the estimated inventory cost. In this case, the income statement will go from January 1, 2012 until June 30, 2012.

Some of the numbers that we need are easily obtained from sales records, customers, suppliers, earlier financial statements, etc. For example, sales for the first half of the year 2012 are taken from the company's records. The beginning inventory amount is the ending inventory reported on the December 31, 2011 balance sheet. The purchases information for the first half of 2012 is available from the company's records or its suppliers. The amounts that we have available are written in italics in the following partial income statement:

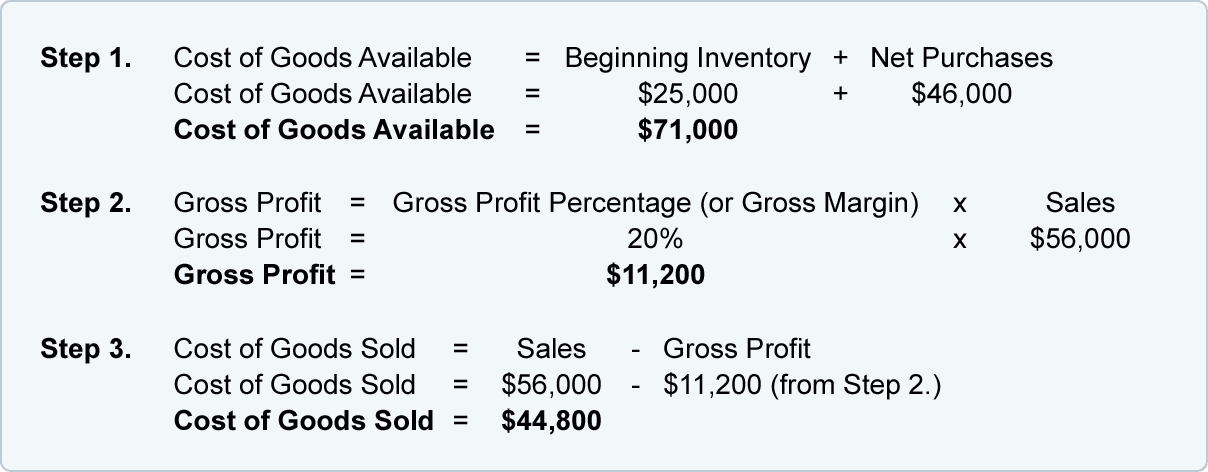

We will fill in the rest of the statement with the answers to the following calculations. The amounts in italics come from the statement above. The bold amount is the answer or result of the calculation.

This can also be calculated as 80% x Sales of $56,000 = $44,800.

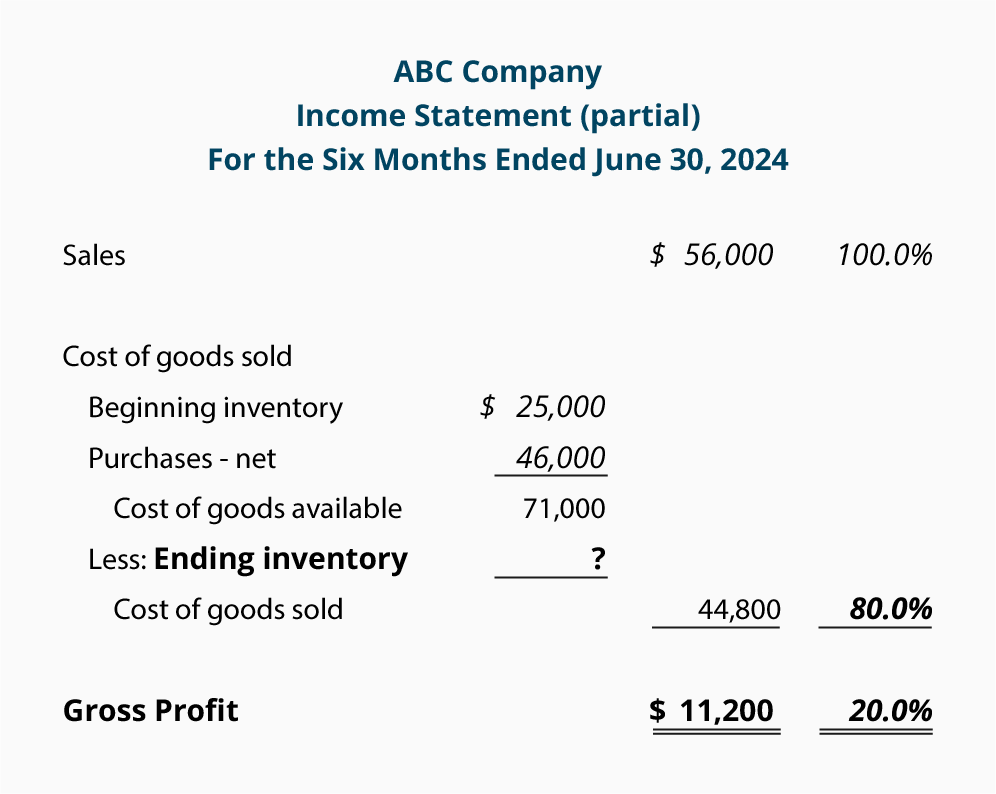

Inserting this information into the income statement yields the following:

As you can see, the ending inventory amount is not yet shown. We compute this amount by subtracting cost of goods sold from the cost of goods available:

Below is the completed partial income statement with the estimated amount of ending inventory at $26,200. (Note: It is always a good idea to recheck the math on the income statement to be certain you computed the amounts correctly.)

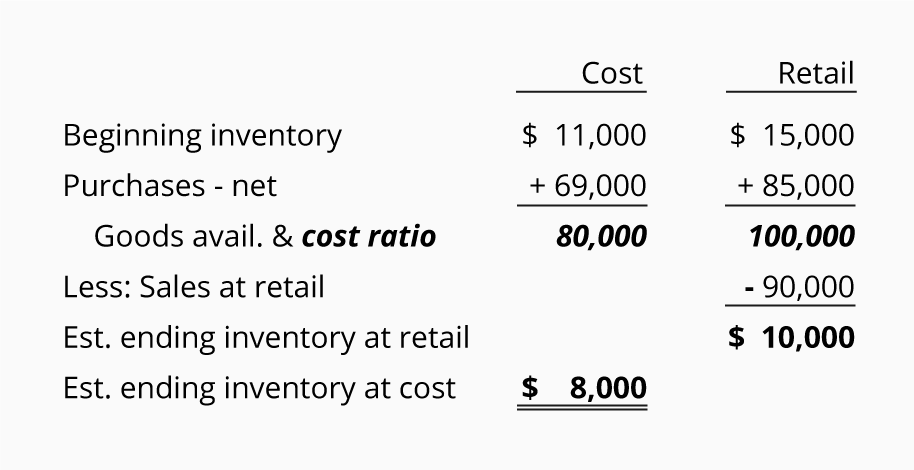

2. Retail Method. The retail method can be used by retailers who have their merchandise records in both cost and retail selling prices. A very simple illustration for using the retail method to estimate inventory is shown here:

As you can see, the cost amounts are arranged into one column. The retail amounts are listed in a separate column. The Goods Available amounts are used to compute the cost-to-retail ratio. In this case the cost of goods available of $80,000 is divided by the retail amount of goods available ($100,000). This results in a cost-to-retail ratio, or cost ratio, of 80%.

To arrive at the estimated ending inventory at cost, we multiply the estimated ending inventory at retail ($10,000) times the cost ratio of 80% to arrive at $8,000.

Additional Information and Resources

Because the material covered here is considered an introduction to this topic, many complexities have been omitted. You should always consult with an accounting professional for assistance with your own specific circumstances.

No comments:

Post a Comment