Cash Flow Statement

.jpg)

While the balance sheet and the income statement are the most frequently referenced financial statements, the statement of cash flows or cash flow statement is a very important financial statement.

The cash flow statement is important because the income statement and balance sheet are normally prepared using the accrual method of accounting. Hence the revenues reported on the income statement were earned but the company may not have received the money from its customers. (Many times companies allow customers to pay in 30 days or 60 days and often customers pay later than the agreed upon terms.) Similarly the expenses that are reported on the income statement have occurred, but the company may not have paid for the expense in the same period. In order to understand how cash has changed, and because many believe that "cash is king" the cash flow statement should be distributed and read at the same time as the income statement and balance sheet.

Format of the Cash Flow Statement

Within the cash flow statement, the cash receipts or cash inflows are reported as positiveamounts. The cash paid out or cash outflows are reported as negative amounts.

The following table provides various ways for you to think of the positive and negative amounts that are shown on the cash flow statement:

The net total of all of the positive and negative amounts reported on the cash flow statement should equal the change in the amount of the company's cash and cash equivalents. (The company's cash and cash equivalents are reported on its balance sheets.)

The cash inflows and cash outflows which explain the change in a company's cash and cash equivalents are reported in three main sections of the cash flow statement:

- Operating activities

- Investing activities

- Financing activities

In addition to the three main sections, the cash flow statement requires the following disclosures:

- the amount of interest paid

- the amount of income taxes paid

- exchanges of major items that did not involve cash (such as exchanging land for common stock, converting bonds into common stock, etc.).

1. Operating activities

The cash flows reported in the operating activities section of the cash flow statement can be presented using one of two methods:

The cash flows reported in the operating activities section of the cash flow statement can be presented using one of two methods:

- Direct method

- Indirect method

The direct method is recommended by the FASB. However, a survey of 500 annual reports of large U.S. corporations revealed that only about 1% had used the recommended direct method. Nearly all of the U.S. corporations in the survey used the indirect method. Hence, we will limit our discussion to the indirect method.

Indirect method, Cash Flows from Operating Activities

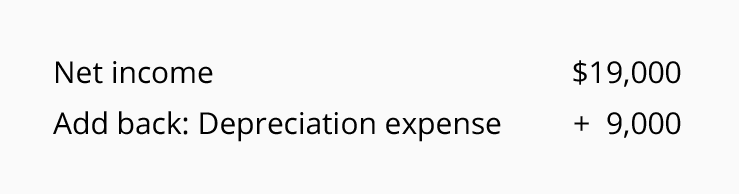

When the indirect method is used, the first section of the cash flow statement, Cash Flows from Operating Activities, begins with the company's net income (which is the bottom line of the income statement). Since the net income was computed using the accrual method of accounting, it needs to be adjusted in order to reflect the cash received and paid.

When the indirect method is used, the first section of the cash flow statement, Cash Flows from Operating Activities, begins with the company's net income (which is the bottom line of the income statement). Since the net income was computed using the accrual method of accounting, it needs to be adjusted in order to reflect the cash received and paid.

The very first adjustment involves depreciation. The amount of Depreciation Expense reported on the income statement had reduced the company's net income, but the depreciation entry did not involve cash. (The journal entry for the current period's depreciation was a debit to Depreciation Expense and a credit to Accumulated Depreciation. Cash was not used.) Since the depreciation expense reduced net income, but did not use any cash, the amount of depreciation expense is added back to the net income amount.

So far, the Cash Flows from Operating Activities is $28,000

Any amortization or depletion expense is also added back.

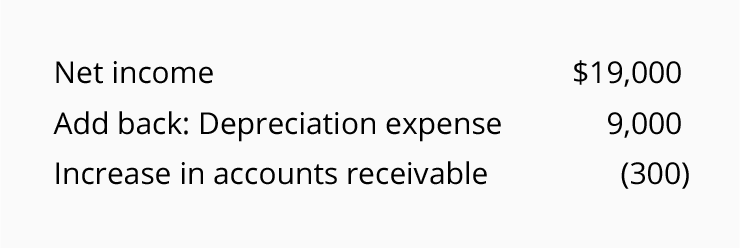

Next, the operating activities will adjust the net income to reflect the changes in the amounts of current assets and current liabilities during the accounting period. For example, if accounts receivable increased from $9,500 to $9,800 during the period, we conclude that the company did not collect cash for all of the sales revenues shown on the income statement. Not collecting all of the sales amounts (or seeing accounts receivable increase) is viewed as negative for the company's cash. Hence the $300 increase in accounts receivable is shown as a negative adjustment of $300:

So far, the Cash Flows from Operating Activities is $27,700

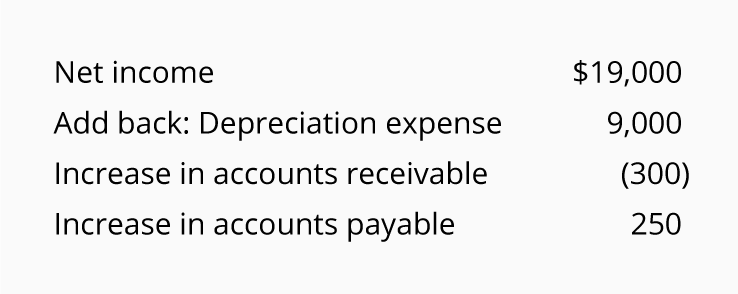

If accounts payable increased from $3,100 to $3,350 during the period, that indicates that the company did not pay all of its expenses. Not paying the bills is good for the company's cash. Hence, the $250 increase in accounts payable will be shown as a positive amount:

So far, the Cash Flows from Operating Activities is $27,950

The changes in the current asset and the current liability accounts are reported as adjustments to the company's net income in the operating activities section—except that the change in short-term notes payable will be reported in the financing activities section.

2. Investing activities

The purchasing and selling of long-term assets are reported in the second section of the cash flow statement, investing activities.

The purchasing and selling of long-term assets are reported in the second section of the cash flow statement, investing activities.

The cash flows that involve long-term assets include:

- The cash received from selling long-term assets. These are reported as positiveamounts.

- The cash used to purchase long-term assets. These are reported as negative amounts.

3. Financing activities

The changes in the noncurrent liabilities, stockholders' (or owner's) equity, and short-term loans are reported in the financing activities section of the cash flow statement.

The changes in the noncurrent liabilities, stockholders' (or owner's) equity, and short-term loans are reported in the financing activities section of the cash flow statement.

The positive amounts in the financing activities section could indicate that cash was received from:

- Issuing bonds payable

- Borrowing through other long-term loans

- Issuing shares of stock

- Borrowing through short-term loans

The negative amounts indicate that cash was used for:

- Retiring (paying off) long-term debt

- Purchasing shares of the company's stock (treasury stock)

- Paying dividends to stockholders

- Repaying short-term loans

Other

At the bottom of the cash flow statement, the net totals of the three sections are reconciled with the change in the cash and cash equivalents that are reported on the company's balance sheet.

At the bottom of the cash flow statement, the net totals of the three sections are reconciled with the change in the cash and cash equivalents that are reported on the company's balance sheet.

The reporting requirements for the cash flow statement also include disclosing the amounts paid for interest and income taxes and significant noncash investing and financing activities. (Two examples of noncash investing and financing activities are converting bonds to common stock and exchanging bonds payable for land.) source

No comments:

Post a Comment