Double-Entry

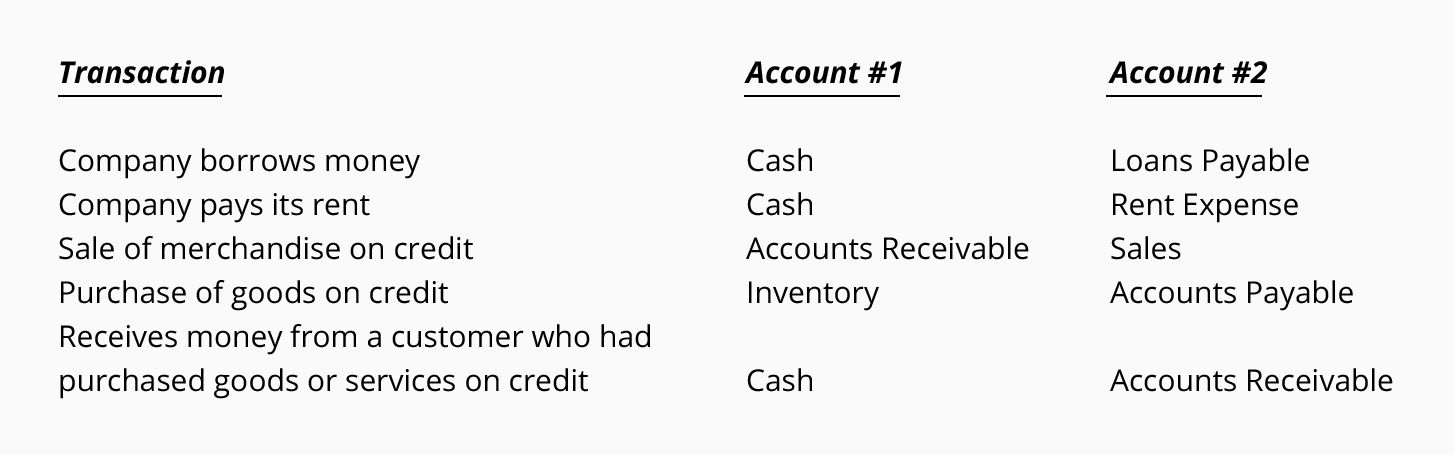

Except for some very small companies, the standard method for recording transactions is double-entry. Double-entry bookkeeping or double-entry accounting means that every transaction will involve at least two accounts. To illustrate, here are a few transactions and the two accounts that will be affected:

Note: Double-entry bookkeeping means that every transaction will involve a minimum of two accounts.

Debits and Credits

The words debit and credit have been associated with double-entry bookkeeping and accounting for more than 500 years. Here are the meanings of those words:

debit: an entry on the left side of an accountcredit: an entry on the right side of an account

The debit and credit rule in double-entry bookkeeping can be stated several ways:

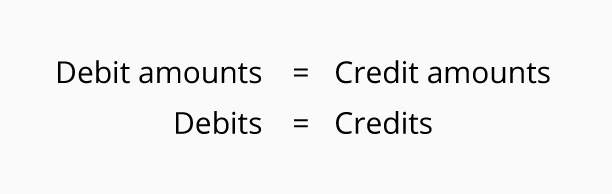

- For each and every transaction, the total amount entered on the left side of an account (or accounts) must be equal to the total amount entered on the right side of another account (or accounts).

- For each and every transaction, the total of the debit amounts must be equal to the total of the credit amounts.

- Debits must equal credits.

In short...

Dependable accounting software will be written/coded to enforce the rule of debits equal to credits. In other words, a transaction will be accepted and processed only if the amount of the debits is equal to the amount of the credits.

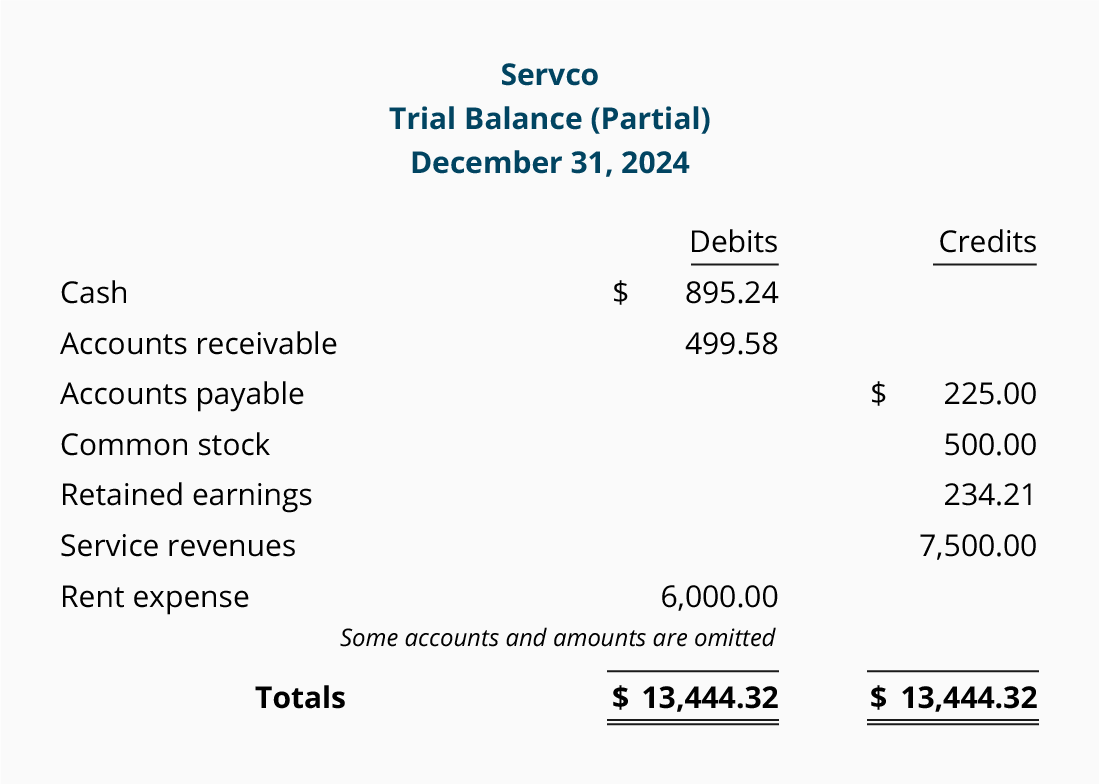

The accuracy of accounting software will also ensure that the accounts and the trial balance will always be in balance. Here is an example of a partial trial balance:

Even though the accounting software has eliminated the clerical errors that occurred because amounts were handwritten and the account balances were calculated manually, some other errors can still occur. Here are some errors that will not be detected by the accounting software:

- An entire transaction (both the debit amount and the credit amount) was omitted.

- An entire transaction was entered twice.

- An incorrect amount was entered both as a debit and as a credit.

- An incorrect account was debited.

- An incorrect account was credited.

Even with the above errors, the trial balance will remain in balance. The reason is that the total of the debit balances will still be equal to the total of the credit balances.

T-Accounts

To assist in visualizing the effect of recording a debit or credit amount and the resulting balances of general ledger accounts, it is helpful to draw a T-account, as shown here:

Debit amounts will be entered on the left side of the T-account, and credit amounts will be entered on the right side. The title of the account will appear at the top of each "T".

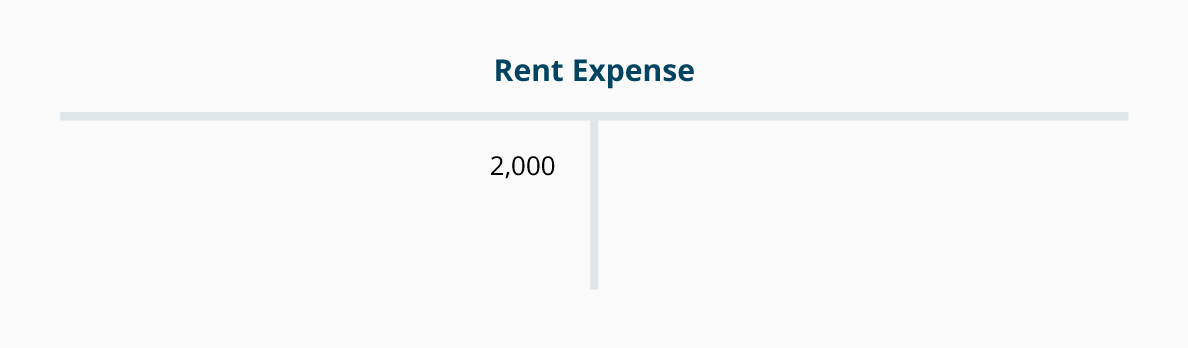

Since every transaction will involve at least two accounts, we recommend that you always begin by drawing two T-accounts. For example, if a company pays its rent of $2,000 for the current month, the transaction could be depicted with the following T-accounts:

Note that one T-account (Rent Expense) has a debit of 2,000 and that one T-account (Cash) has a credit amount of 2,000. Hence, the transaction had debits equal to credits.

No comments:

Post a Comment